Leveraging shareholder data for beneficial ownership transparency

Fragmentation in company ownership data systems

Information about legal entities in shareholder data and BO declarations show related aspects of corporate networks. Beneficial ownership refers to the natural person(s) who ultimately own, control, or benefit from a legal vehicle, including through indirect or non–share-based means. Shareholder data records the direct, legal owners of shares, who may be natural persons or legal vehicles. Generally, the objectives of these registers may be different. For example, shareholder registers may be under the general purview of a company registrar executing its mandate, while BO registers may be implemented for specific policy purposes, such as anti-money laundering (AML).

The owning of shares applies to companies as well as some other types of legal vehicles. [4] A shareholder is an individual or legal entity that owns at least one share of a company’s stock. Shareholders essentially own the company, and this comes with the right to share in the profits. [5] While in some jurisdictions shareholder data is held by the companies themselves, in others this information may be centrally held by a company registrar. [6] The time period within which shareholder information is or needs to be updated, and how the information is stored, its legal significance, differs across jurisdictions. For example, in the United Kingdom (UK), shareholder information is updated annually and is accessible via a PDF. In Zambia, information needs to be updated immediately upon share transfer, and it is held as structured data. In Pakistan, there is a proposal for the central shareholder register to become a digital central securities depository, where the registration of shares has a constitutive effect, giving legal certainty over ownership of the shares enabling their trading. [7] However, different legal entities, such as non-profits, may sometimes be registered with different authorities.

A BO register is often overseen by the company registrar, but it may also be maintained by other authorities, such as tax authorities or financial intelligence units. Even where BO information is held by the company registrar, BO reporting obligations may extend to a wider range of legal entities than those covered by the company registrar. BO declaration systems collect varying amounts of information on intermediaries where declared interests are indirect (see Figure 1). This can range from not collecting any information on the indirect relationship, or just collecting the fact of whether the relationship is direct or indirect, to collecting information on some or all of the intermediaries. [8]

A beneficial owner is often defined in regulations as someone who meets one or more of a set of criteria. One such common criteria is controlling ownership of a company through direct or indirect shareholding. This is generally expressed in a percentage – often 25% – although there are many examples of jurisdictions adopting thresholds as low as 5%. [9]

As a result, there are a number of corporate network types where beneficial owners can be determined solely on the basis of domestic records of legal ownership. Of these, the simplest is where a company’s shares are all directly held by individuals. Those individuals whose shareholding exceeds the BO threshold are deemed beneficial owners. Another corporate network in this category is where individuals hold indirect shares above the BO threshold, but all companies in the network are domestic. BO information’s added value is expected to be with more complex networks involving cross-border ownership (in the absence of international data-sharing), legal arrangements, and other forms of influence and control not based on the ownership of shares. These structures are of particular interest for tackling crime.

Shareholder data also provides additional granularity where share ownership is below the legal threshold for beneficial ownership, which means it is not included in BO information. By contrast, BO information will also include information about parties with non-share-based interests, or where ownership is held indirectly by shares through a foreign legal vehicle (see Figure 1).

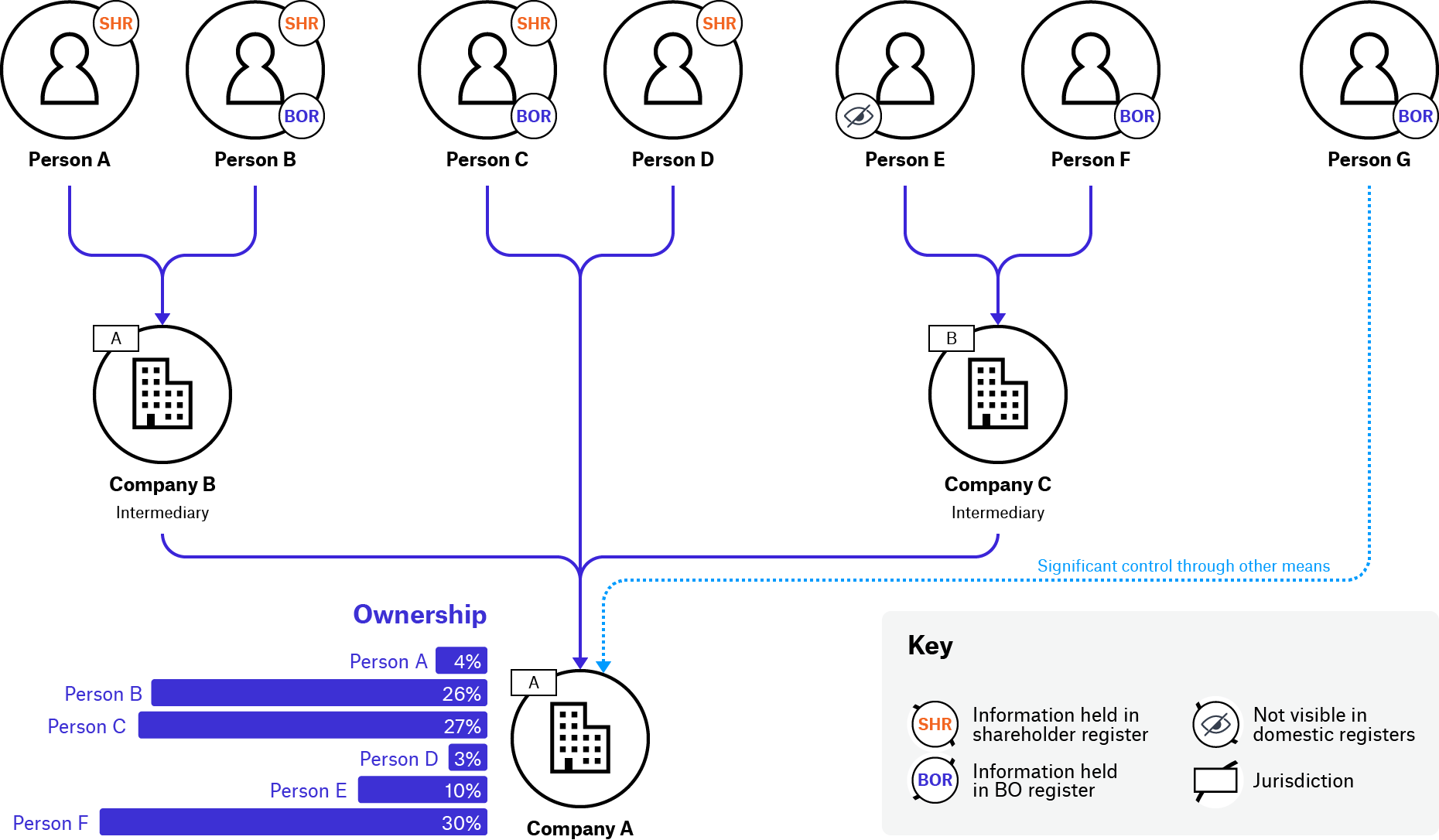

Figure 1. Illustrative example of a corporate network revealed through domestic beneficial ownership and shareholder data (25% threshold)

In this corporate network, Company A’s shares are directly owned by two companies: Company B (both registered in Jurisdiction A) and Company C (registered in foreign Jurisdiction B); and two individuals: Person C and Person D. Person A and Person B own shares in Company A indirectly via Company B, while Person E and Person F do so through Company C, making both Company B and Company C intermediaries in the network. Person G exercises significant control through other means over Company A. Depending on the nature of the interest (i.e. share ownership or other forms of control) and the level of ownership (i.e. percentage of shares owned), individuals and entities may appear in the domestic shareholder register, BO register, or both. Information can be combined from these sources to reveal this network. For example, Person F is identified in BO data because their ownership exceeds the 25% threshold, whereas Person E is not visible, as their shares are held through a foreign entity and fall below the threshold.

Despite this complementarity, shareholder and BO registers are often treated as separate and disconnected data sources. Jurisdictions implementing BO registers for legal vehicles may start from scratch, when in reality they may already be holding relevant information. This creates uncertainty around how the two datasets relate in practice, how much BO information is already observable through shareholder data, and where the two diverge.

These considerations are also critical for facilitating cross-border data use and international data-sharing, particularly in identifying transnational ownership structures that cannot be fully understood within a single jurisdiction and enabling ownership information from different sources to be meaningfully combined and analysed.

Footnotes

[4] For example, associations and partnerships in some jurisdictions. For simplicity, this paper will at times refer to “companies”.

[5] Adam Hayes, “Shareholder Definition: Rights & Types Explained”, Investopedia, updated 2 April 2026, https://www.investopedia.com/terms/s/shareholder.asp.

[6] For example, Australia, Austria, Belgium, China, Denmark, France, Germany, Greece, Ireland, Italy, Japan, Malaysia, Malta, the Netherlands, New Zealand, Singapore, and the UK.

[7] For example, Pakistan: SECP, “SECP Approves Full Digitization of Share Ownership for Unlisted Companies to Enhance Transparency and Investor Protection”, LinkedIn, March 2026, https://www.linkedin.com/posts/secp-approves-full-digitization-of-share-share-7430522635597402112-b1Zt.

[8] For example, the UK does not state whether the relationship is held directly or indirectly. South Africa collects information on the parent of a declaring company in an indirect relationship. Armenia collects information about all intermediaries in an indirect relationship.

[9] For example, Nigeria. The maximum threshold stipulated by the FATF is 25%. See: FATF, International Standards on Combating Money Laundering and the Financing of Terrorism & Proliferation: The FATF Recommendations (FATF, updated 2025), 96, https://www.fatf-gafi.org/content/dam/fatf-gafi/recommendations/FATF%20Recommendations%202012.pdf.coredownload.inline.pdf.